Test your stock investing knowledge using our innovative online calculator. It’s a test designed using 28 comprehensive questions. This interactive tool provides a personalized evaluation of your stock investing skills. From basic concepts to complex analysis, challenge yourself and receive a percentage score that reflects your expertise. You can use this calculator to quantify the extent of your knowledge of stocks.

In the dynamic world of stock investing, having a solid understanding of stocks and the market is essential. It will help to make informed investment decisions. That’s where online calculators like these play a crucial role.

These calculators provide individuals, like yourself, with a quantifiable measure of their stock investing knowledge. One of the primary reasons why such calculators are required is to evaluate the depth and breadth of one’s stock investing knowledge. They offer an opportunity for self-assessment, allowing individuals to gauge their expertise and identify areas where further learning and improvement is needed.

In the fast-paced and ever-evolving world of stock investing, knowledge is power. The importance of having a solid understanding of stocks, markets, and investment strategies cannot be overstated. It is the bedrock upon which successful investment decisions are made and can have a profound impact on one’s financial well-being.

Recognizing this significance, we present an article that delves into the realm of stock investing knowledge. We are also offering a unique tool to assess and quantify your understanding of stock investing: the StockInvest IQ calculator.

Through a series of carefully crafted questions, this calculator will assess your grasp of essential concepts, analytical techniques, and risk management strategies.

Stock investing is a popular and potentially lucrative way to grow wealth and achieve financial freedom. However, it requires a solid understanding of the basics. Careful consideration of the potential benefits and risks involved is also necessary.

Let’s explore the fundamentals of stock investing, including what stocks are and how they work.

Stock investing involves buying shares or ownership stakes in publicly traded companies. When you purchase a stock, you become a shareholder and have a claim on the company’s assets and earnings.

Stocks are typically traded on stock exchanges, such as the Bombay Stock Exchange (BSE) or National Stock Exchange (NSE). Here the buyers and sellers come together to execute transactions. Know more about the stock market from here.

The primary goal of stock investing is to generate a return on investment (ROI). This can occur in two ways. First is through capital appreciation, where the stock price increases over time. The second is through dividends, which are a portion of the company’s profits distributed to shareholders.

Investors choose to hold stocks for the long term. They aim to benefit from the company’s growth and increase in value. A few known investors are Warren Buffett, Peter Lynch, Late Rakesh Jhunjhunwala, etc. Check 5 Golden Rules of Stock Investing.

People can also engage in short-term trading to take advantage of price fluctuations. These people are called traders, they are not investors but speculators. Though it is also true that very trained speculators can also make money from stock trading.

It is also crucial to acknowledge the risks associated with stock investing.

Prices of most stocks remain very volatile. The price is influenced by various factors such as economic conditions, market sentiment, and company-specific events. There is always the possibility of making a loss in stock investing. If the company performs poorly or goes bankrupt, the risk of loss is very high. For such companies, the stock price can crash very fast.

Even surrounding conditions can influence the price of individual stocks. Like it happened during the subprime mortgage crisis (2008-09), Brexit, and Covid-19 (2020). Global factors can cause fluctuations that impact stock prices. The challenge is to learn to time the market which is really challenging task and for most people, it is also impossible.

Having a solid understanding of stock investing is paramount for individuals seeking to build long-term wealth. Knowledge is the foundation upon which successful investment decisions are made. It plays a pivotal role in shaping an investor’s journey.

Let’s delve into the significance of stock investing knowledge and how it can positively impact investors.

A key benefit of stock investing knowledge is the ability to analyze stocks effectively. Investors equipped with the necessary knowledge can read and interpret financial statements. This helps in the evaluation of the company’s fundamentals and in formulating key financial ratios.

It enables the person to make informed judgments about a company’s value, growth prospects, and financial health.

A deep understanding of fundamental analysis techniques equips investors to identify high-quality stocks and make sound investment decisions.

Stock investing knowledge empowers investors to spot investment opportunities that may be overlooked by others. It can be done by staying informed about market trends, industry developments, and emerging sectors.

This is the way knowledgeable investors can identify undervalued stocks or companies with strong growth potential.

This insight enables them to capitalize on market inefficiencies and potentially achieve superior investment returns.

The stock market is inherently unpredictable, and risks abound. However, investors armed with stock investing knowledge are better equipped to manage and mitigate these risks.

How to mitigate the risks? Through proper risk assessment, portfolio diversification, and an understanding of different investment strategies. This way, knowledgeable investors can construct a well-balanced portfolio that aligns with their risk tolerance and investment objectives.

Additionally, knowledge enables investors to identify warning signs and indicators of potential market downturns. It insight allows them to make informed decisions to protect their investments.

Stock investing knowledge is not static; it requires ongoing learning and adaptation. The market landscape evolves, new investment instruments emerge, and regulations change. Investors who prioritize knowledge are better prepared to adapt to these changes and refine their strategies as needed.

By staying informed through reading or seeking advice from professionals, investors can continually enhance their stock investing knowledge. This way they continually improve their decision-making abilities.

Knowledge enhancement is a must in stock investing. One cannot afford to cling only to the old theories and practices. Though the age-old value investing theories of Benjamin Graham is still relevant, new investing skills will assist further.

Enhancing stock investing knowledge is a continuous process that can significantly benefit investors in making informed decisions and achieving better investment outcomes.

In this section, we will explore some practical steps and recommend valuable resources to aid in your learning journey.

Refer to Online Portals: There are websites such as Investopedia and Morningstar that offer a vast array of articles, tutorials, and market analysis. Subscribe to their newsletters or follow their social media channels to receive updates. You can also follow this blog on Twitter and Telegram.

Use Online Tools: You can also use an online tool like our Stock Engine. It can help one to screen potential stocks and provide a report on individual stocks. It is basically a fundamental analysis tool. Apps like these provide updated information and analysis about stocks.

Continuous learning and practiceare key to improving stock investing knowledge. It’s important to apply what you learn. Try to do your own analysis and buy a stock. The whole process of analysis, buying, and holding will give you a different perspective of stock investing.

By taking the assessment, readers can gauge their understanding of various concepts and identify potential gaps in their knowledge. This self-assessment tool serves as a valuable starting point for further learning and growth.

“Pricing power is the ultimate business superpower. It allows companies to dictate their own terms, maintain healthy profit margins, and withstand competitive storms. Companies with pricing power are basically businesses with amonopoly status. Such companies display great brand strength to market dominance.”

In this article, we unravel the mysteries of pricing power. We’ll explore how it can make or break companies. We’ll discuss why investors and business owners alike should pay keen attention to this invaluable asset.

Pricing power refers to a company’s ability to adjust prices without a significant impact on demand. Such an action enables it to maintain higher profit margins and withstand competitive pressures. It ultimately drives long-term profitability. Hence, Understanding and assessing pricing power is crucial for investors and businesses.

“Unleashing the Power of Pricing: How Pricing Power Drives Business Success” is likely the title or topic of a book, article, or discussion that explores the critical role of pricing strategies in business success. While I don’t have access to specific content beyond my knowledge cutoff date in September 2021, I can provide you with a general overview of the concept and the importance of pricing power in business:

Pricing Power Definition: Pricing power refers to a business’s ability to set and maintain prices for its products or services at levels that are profitable and sustainable. A company with strong pricing power can influence and control pricing in its market, often due to factors such as brand strength, product differentiation, or a loyal customer base.

Profitability: Pricing power enables a business to charge higher prices for its products or services, resulting in increased profitability and revenue.

Competitive Advantage: Companies with pricing power can withstand competitive pressures and market fluctuations more effectively. They are less vulnerable to price wars and can maintain healthy profit margins.

Brand and Perceived Value: Strong brands and products with unique features or perceived high value often command higher prices. Customers are willing to pay more for products they perceive as superior.

Customer Loyalty: Building strong customer loyalty allows a company to maintain pricing power. Loyal customers are often less price-sensitive and more willing to pay premium prices.

Innovation: Continuously innovating and offering unique products or services can help a business establish and maintain pricing power. Customers are willing to pay more for innovative solutions.

Segmentation: Effective pricing strategies often involve segmenting the market and offering different price points for different customer segments. This allows a business to capture value from various customer groups.

Value-Based Pricing: Pricing based on the perceived value of a product or service to the customer is a powerful strategy. It aligns pricing with what customers are willing to pay.

Elasticity: Understanding price elasticity of demand (how sensitive customers are to price changes) is crucial. Businesses with pricing power can often raise prices without significant loss of sales volume.

Data and Analytics: Modern businesses leverage data and analytics to fine-tune their pricing strategies. This helps in optimizing prices for maximum profitability.

Ethical Considerations: While pricing power can lead to higher profits, businesses must also consider ethical implications and avoid price gouging or unfair practices.

In essence, the concept of pricing power underscores the importance of pricing as a strategic tool in business. When leveraged effectively, it can be a driver of long-term success by enhancing profitability, market position, and customer loyalty. Books, articles, and discussions on this topic often delve into case studies, real-world examples, and actionable strategies for businesses to develop and utilize pricing power to their advantage.

Warren Buffett, one of the most successful investors of all time and the chairman and CEO of Berkshire Hathaway, has frequently emphasized the importance of pricing power in his investment philosophy and business strategy. Here are some key insights and quotes from Warren Buffett regarding pricing power:

In this quote, Buffett highlights that a business with pricing power can increase prices and maintain or even grow its customer base, which is a sign of a strong and resilient business model.

Buffett’s ideal business is one that not only has pricing power but also can reinvest its profits at high returns. This combination leads to compounding growth in value over time.

Buffett emphasizes that a business’s ability to generate high returns on invested capital is a key factor in its long-term success. Pricing power plays a crucial role in achieving those high returns.

**”You want to be able to charge prices that reflect the value you’re providing. If you’ve got a good product or service and you’ve got the ability as a result of uniqueness or geographic location or whatever it may be to charge a price that is commensurate with the utility you’re giving people, you’re in a great position as a business.”

Buffett underscores that pricing should align with the value a business provides to its customers. If the product or service is valuable and unique, the business can command higher prices.

While not explicitly about pricing power, this quote highlights Buffett’s focus on identifying businesses with a sustainable competitive advantage. Pricing power often contributes to a company’s competitive advantage by allowing it to maintain superior profitability.

In summary, Warren Buffett recognizes the significance of pricing power in assessing the quality of a business and its potential for long-term success. A company with pricing power can maintain or increase prices while delivering value to customers, resulting in strong and enduring financial performance.

In that letter, he emphasized the significance of pricing power as a key factor in evaluating businesses. He highlighted its crucial role in determining a company’s competitive advantage and long-term profitability. Since then, Buffett has consistently referenced and emphasized the importance of pricing power in various shareholder letters, interviews, and public discussions on investing and business strategy.

Pricing power is a concept that encapsulates a company’s ability to set prices for its products or services, without resistance. Normal companies (with no pricing power) experience significant resistance when they try to hike prices. The price hikes impact customer demand.

Understanding and assessing pricing power is crucial for investors and businesses alike. It directly affects a company’s ability to generate sustainable profits, maintain market share, and withstand competitive pressures.

By identifying companies with strong pricing power, investors can make informed decisions to maximize potential returns. The businesses can also leverage this advantage to solidify their market position and drive long-term growth.

Market dominance plays a significant role in shaping the pricing power of companies. When a company holds a substantial market share, it often gains a greater ability to influence and control prices. Here are a few more factors that can influence the pricing power:

Unique Offering: Such companies often offer unique products or services. This is what gives them a dominant market position. Their ability to offer something unique allows them to ask for higher prices than their competition. The customers also pay a premium for the perceived value they receive.

Brand Loyalty: The pricing power is bolstered by strong brand recognition and customer loyalty. When customers associate a brand with quality or desirability, they are more likely to accept higher prices without seeking alternatives.

Monopoly Status: Such companies benefit from limited substitutes or alternatives available to customers. This situation gives a kind of monopoly status to companies. Hence, coherent price rises are often acceptable to the customers.

Dominant Player: They have more pricing power than competitors. Such companies create higher barriers to entry. The entry barrier is created by economies of scale, strong brand recognition, high customer switching costs, or established distribution networks.

Nonetheless, market dominance generally provides companies with a stronger position to dictate prices. These companies can also resist price pressure from competitors, and maintain their higher profit margins.

To develop and enhance pricing power, companies can employ several strategies. We’ll discuss some of them in this article. Though it is not an exclusive list this is what I’ve observed by looking at companies with pricing powers.

Differentiation and Value Proposition: Companies can develop pricing power by offering unique products or services. Feature-rich offering which is also of superior quality, or innovative is my first choice. For example, Apple Inc clearly delivers the value proposition through its products. This way it can differentiate itself from competitors and justify premium pricing.

Branding and Reputation Building: Building a strong brand and reputation establishes trust, credibility, and customer loyalty. It enables companies to command higher prices. Investing in brand-building activities, effective marketing campaigns, and consistent customer experiences can enhance pricing power. Again, Apple Inc has mastered the art of brand building.

Customer Relationship: Nurturing strong customer relationships is crucial for pricing power. Companies offering premium products backed by excellent service build strong brand loyalty. Loyal customers often resubscribe and are ready to pay increased prices if any.

Continuous Innovation: Investing in continuous innovation and product development helps companies stay ahead of the competition and maintain pricing power. By regularly introducing new features, improvements, or product lines, companies can justify premium pricing and avoid commoditization.

Operational Excellence and Cost Efficiency: Efficient operations and cost management contribute to pricing power. Companies that optimize their supply chain and have a streamlined process can practice higher pricing power. Companies that can leverage economies of scale can offer competitive prices and can still maintain profitability. The cost advantages provide flexibility in pricing decisions.

By implementing these strategies and continuously adapting to market conditions, companies can strengthen their pricing power.

Pricing power serves as a crucial driver of long-term success and resilience in the ever-evolving business landscape.

In the large-cap space, there are companies like Asian Paints, Nestle India, HUL, and Titan Company that display phenomenal pricing power.

But there are few companies from the mid and small-cap spacethat has displayed signs of pricing power.

Relaxo Footwear: As of June-2023, its market cap is about Rs.22,600 crore. It is a leading footwear company in India. It has a strong brand presence and reasonable product quality. The company has successfully established itself as a premium brand in the affordable and mid-price range footwear segment. Relaxo Footwear has been able to maintain higher price points compared to its competitors, reflecting its pricing power in the market. The company’s wide distribution network and market penetration have contributed to its pricing power. The P/E ratio of Relaxo is 144. Check its fundamentals here.

India Nippon Electricals: As of June-2023, its market cap is about Rs.1,020 crore. It is a leading manufacturer of ignition systems for automotive and general-purpose engines. In recent years, the company has been able to raise prices without losing too many customers. This is due to the high quality of its products and the lack of substitutes available in the market. The P/E ratio of India Nippon is 21.15. Check its fundamentals here.

Chemcon Speciality Chem: As of June-2023, its market cap is about Rs.1,017 crore. This company is a leading manufacturer of specialty chemicals. It has a strong brand reputation and a large market share in the domestic market. Over the last five years, the ROE and ROCE of the company have been trading above 15% and 20% levels respectively. The P/E ratio of Chemcon is 18.5. Check its fundamentals here.

Ksolves India. As of June-2023, its market cap is about Rs.1,065 crore. This company is a leading provider of IT solutions in India. In the last three years, the company is able to increase its ROE and ROCE at a dramatic pace. In the last three years, its operating revenue and net profit have increased by three folds. Though equity has also got diluted by almost 8 times.

Till the company is enjoying the pricing power, it looks invincible. But it must also be considered that no company can have the pricing power forever. There will be new companies coming in that will eventually break their economic moat.

Here are some key considerations:

The elasticity of Demand: Pricing power assumes that customers will accept higher prices without significantly reducing their demand. However, if the price increase is met with a more significant decline in demand than anticipated, it can result in lost sales and revenue. Companies need to carefully assess price sensitivity. Otherwise, if they overestimate their pricing power, they may end up losing their market share.

Competitive Pressure: Pricing power can be challenged by intense competition in the market. Competitors may respond to price increases by offering lower prices, promotional offers, or alternative products. This can erode a company’s pricing power and force them to adjust their pricing strategy to remain competitive.

Market Disruption and Technological Advances: Disruptive technologies or market shifts can quickly undermine pricing power. Companies that fail to adapt to changing market dynamics or technological advancements may find their pricing power diminished.

Regulatory and Legal Constraints: Pricing decisions may be subject to regulatory oversight or legal constraints. For example, companies operating in sectors like oil & gas, power, utilities, banking, Airlines, Telecom, etc can have only little or no pricing power.

Customer Perception and Brand Equity: Pricing power relies heavily on customer perception and the perceived value of a company’s products or services. If customers perceive a mismatch between the price and the value they receive, it can undermine pricing power. If customer trust and loyalty get eroded, pricing power will also vanish.

Economic Factors: Economic downturns, inflation, or changes in consumer purchasing power can impact pricing power. In times of economic or geo-political instability, companies find it hard to maintain their power of pricing.

Pricing power is a crucial aspect for investors to consider when evaluating potential investment opportunities. Companies with strong pricing power possess a unique advantage that allows them to command higher prices, maintain profit margins, and withstand competitive pressures.

Operating Profit Margin: This metric measures the profitability of a company’s core operations. A higher operating profit margin (OPM) implies that the company has effective cost management. A consistently high OPM suggests that the company has pricing power.

Relative Margins & Revenue: Comparing a company’s GPM and OPM with its peers can build a strong impression of the company’s pricing power. If the margins of the company are growing at a rate faster than its peers, it is a big advantage. But while making this analysis, it is also essential to look at operating revenue growth. If the revenue is also growing faster than the peers, it is a clear sign of pricing power.

Companies with strong pricing power can command higher prices, maintain profit margins, and withstand competition. By identifying companies with high pricing power, investors can make informed investment decisions. This way they can benefit from their sustained profitability and competitive advantage.

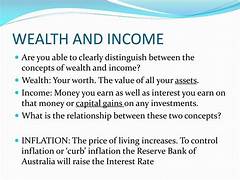

Income and wealth are two distinct concepts in personal finance. Income refers to the money earned regularly, while wealth represents the accumulated assets and net worth. Understanding the difference between income and wealth is vital for effective financial planning. It guides budgeting, investment decisions, and long-term wealth-building strategies.

When it comes to personal finance, the terms “income” and “wealth” are often used interchangeably. However, they represent distinct concepts that play a crucial role in one’s financial journey. Income refers to the money earned regularly, whether through employment, investments, or other sources. On the other hand, wealth encompasses the accumulated assets and net worth of an individual or entity.

Differentiating between income and wealth is important. It helps individuals understand their financial situation more accurately and make informed decisions.

Many people mistakenly assume that a high salary automatically translates into high wealth. However, this is not always the case. Here’s why:

Expenses and Lifestyle: A high-salary earner may have significant expenses and a lavish lifestyle. Such a lifestyle is supported by their high income. A significant portion of their income goes towards maintaining their lifestyle. As a result, they may end up saving and investing less. Only significant investments can lead to wealth creation.

Overspending Using Debt: Some high-salary earners may carry significant loans. Why? Because they can afford to pay the monthly EMIs. They wrongly correlate their EMI paying ability with their affordability. Suppose, my monthly salary is such that I can easily pay one lakh in EMI. As a result, I will assume that I can easily buy a home worth one crore (assuming, a 1 Crore loan = 1 lakh EMI). But in reality, my bank balance was only five lakhs. It means, what I’m assuming is affordable is a fallacy.

[P.Note: Individuals with moderate incomes can accumulate significant wealth. If they practice diligent saving, make wise investment choices, and manage their expenses effectively, they can also become wealthy. Wealth is built over time through a combination of income, savings, investment growth, and debt management.]

The Definition of “Wealthy” in India

I have a theory that I use to distinguish a normal person from a wealthy person.

As per data published by the World of Statistics, on average, professionals in Indiaearn an income of about Rs.46,900 per month. We’ll use this figure as our basis to define who is wealthy in India. Please note that I’m assuming Rs.46,900 as the net take-home salary and not the CTC (Cost to the Company). It means Rs.46,900 is the amount that gets credited to one’s bank account each month.

Let’s define the minimum characteristics of a wealthy Indian person. A person who is starting to show these first characteristics is beginning to become wealthy.

Characteristic #1 (Earned Income): The minimum earned income of the person should be at least two times the average world data (Rs.46,900). It means, if the person is earning an average take-home salary ofabout Rs.95,000 per month, he is satisfying the first parameter of being wealthy. Please note that by earned income I mean income from job, business, etc.

Characteristic #2 (Passive Income): The minimum passive income of the person should be at least equal to the average world data (Rs.46,900). It means, the person must have an investment portfolio that consists of enough passive-income-generating assets. Assuming an income yield of 6.5% per annum, the size of the asset base should be at least Rs.87,00,000. To know the difference between earned income and passive income, read this article.

Characteristic #3 (Growth Portfolio): There are two components of an investment portfolio. The first takes care of the passive income (#2 above). The second takes care of the necessary growth that makes a person wealthier time after time. The minimum size of this growth portfolio should be at least 50% of the passive income portfolio. As we’ve fixed the minimum asset base in #2 as Rs.87 lakhs, the minimum size of the growth portfolio isRs.45,00,000.

Who can be called as wealthy in India? A person is wealthy if he/she is showing at least these two characteristics in tandem. First, his/her investment portfolio size is at least Rs.1.3 crore. Second, his monthly earned income is at least Rs.95,000 per month.

So, taking this as our basis for being wealthy, let’s try to answer a tricky question.

Suppose there is a fresh graduate (Mr.ABC) whose starting salary is Rs.4,00,000 per month. Can he be treated as a wealthy individual? As we have already seen, to become wealthy, the person must fulfill the following four characteristics.

But a high monthly income can assist in building the required investment portfolio faster. Such a person can also buy a small home as per his affordability very early in life. This way, his path to a wealthy life becomes a tad bit easier.

But I would like to clarify a point here. Here, the above explanation may give the impression that a high paycheck is the only key requirement to becoming wealthy faster. A higher paycheck is certainly helpful, but it does not mean that people with lower incomes cannot become wealthy.

How lower-income people can become wealthy?

Here is an example of two people. First is the high-earning person who makes about Rs. 4 Lakhs per month income. Second is a normal average person who earns an income of about Rs.1 Lakhs per month.

Let’s study these two individual’s investing habits and how it accounts for their long term wealth creation.

High Income (Rs.4 Lakhs / Month): The person invests about Rs.1.5 Lakhs per month. As he is not very conversant with investments, he found it better to invest in a diversified equity mutual fund through the SIP route. This mutual fund scheme yielded a return of close to 16% per annum in 15 years. At the end of the 15th year, he built a corpus of about Rs.11.2 Crores.

Average Income (Rs.1 Lakhs / Month): The person invests about Rs.15,000 per month. The person is conversant with investments, hence he invested directly in quality shares. As this person was wiser in investing, he also started investing five years early than his peer. He very carefully built his stock portfolio which yielded him a return close to 26% per annum in 20 years. At the end of the 20th year, he built a corpus of about Rs.12.0 Crores. Read: Test your knowledge of stocks.

The idea is to use one’s intelligence and knowledge to identify quality stocks. Investing one’s money into such stocks and staying invested for the long term can help one become wealthy over time.

Out of all people in a nation, only a handful of people are rich.

In order to judge how wealthy is a person, we can use this scale to judge the degree of wealth one has accumulated. What is the requirement to be tagged as wealthy? Check here.

Grade 0 – Not meeting the criteria

Grade C – Just Rich (Just meeting the criteria).

Grade B – Moderately Rich (Income and Assets at least 10 times the requirement).

Grade A – Really Rich (Income and Assets at least 50 times the requirement).

Grade A+ – Filthy Rich (Income and Assets at least 100 times the requirement).

While income is important for meeting day-to-day expenses and maintaining a comfortable lifestyle, wealth is more stable and accumulative in nature.

Differentiating between income and wealth is essential to avoid common misconceptions. Simply having a high salary does not guarantee wealth, as expenses, lifestyle choices, and debt can hinder wealth creation. There are people who earn a very high salary but spends all if it on needless things. Such people have no spare money for investment and wealth creation.

It is important to manage expenses effectively, make wise investment choices, and practice diligently saving to build wealth over time.

Moreover, it is essential to recognize that wealth can be achieved by individuals with moderate incomes as well. By making informed financial decisions, focusing on savings, and investing wisely, anyone can accumulate significant wealth.

Higher income can facilitate wealth creation, it is not the sole determining factor. Even individuals with lower incomes can become wealthy by leveraging their investing skills, making informed investment choices, and focusing on long-term growth.

A common misunderstanding between credit and debt is that they are often used interchangeably or considered synonymous. While they are closely related concepts, they have distinct meanings and implications. This article will use examples to explain the difference between credit and debt

Equating credit with debt: Some people mistakenly believe that credit itself is the debt. However, credit refers to the trust or borrowing capacity extended to individuals or entities. Whereas, debt represents the actual financial obligation resulting from utilizing that credit.

Credit is a negative aspect of financial management: Some individuals associate credit with excessive borrowing or being in debt. However, credit, when used responsibly, can be a valuable tool for facilitating economic activities. It is the misuse or mismanagement of credit that can lead to overwhelming debt and financial difficulties.

Being debt-free will get a good credit score: While minimizing debt is generally advisable. But having no credit history can be as damaging as a high debt burden. In a way, credit is an unavoidable requirement for the majority. Keeping oneself creditworthy is also necessary.

The incorrect definition fails to capture the essential aspect of credit, which is the extension of trust and the ability to access funds or goods based on that trust. It wrongly emphasizes the owed amount rather than focusing on the concept of financial trust and the borrowing capacity that credit represents.

Remember, credit is not about the amount owed but rather theability to borrow or accessfunds based on one’s creditworthiness. It’s crucial to understand this distinction to have a clear understanding of credit and its role in financial transactions.

Before we proceed to see the examples, another small clarification about debt.

The other forms of debt borrowing can also arise from other forms of credit, such as credit cards, lines of credit, mortgages, personal loans, or borrowing from individuals, etc.

Imagine you are a member of a community-based library. The library allows its members to borrow books for a certain period. Here’s how credit and debt come into play in this scenario:

As a member of the library, you have access to credit in the form of borrowing books. The library extends credit to you, allowing you to take books home without upfront payment. This credit represents the trust placed in you as a member to borrow books and return them within the specified borrowing period.

When you borrow a book from the library, you incur a debt to the library. This debt represents your obligation to return the book within the agreed-upon timeframe. Until you return the book, you have a debt to the library for that specific item. Once you return the book in good condition, your debt to the library is settled.

Imagine you want to purchase a new smartphone worth ₹50,000, but you don’t have enough money to pay for it upfront. Here’s how credit and debt come into play:

After making the purchase using your credit card, you now have a debt of ₹50,000. This debt is the financial obligation you owe to the credit card company. It represents the amount you borrowed to buy the smartphone. You will need to repay this debt according to the terms and conditions set by the credit card company. If you don’t pay off the debt promptly, it may accrue interest charges, making the total amount owed higher over time.

It’s important to note that credit and debt are intertwined. How? Because credit enables you to incur debt. But it is essential to remember that they are distinct concepts. Credit represents the ability to borrow or access funds, while debt represents the actual obligation resulting from borrowing.

Suppose you are looking to purchase a car worth ₹5,00,000, but you don’t have enough money to buy it outright. Here’s how credit and debt come into play in this scenario:

You approach a bank or a financial institution for a car loan. After reviewing your creditworthiness, income, and other factors, the bank approves your loan application. The bank extends credit to you by granting you a loan of ₹5,00,000. This credit represents the financial trust placed in you to borrow the required amount to purchase the car.

With the approval and disbursement of the loan, you now have a debt of ₹5,00,000. This debt is the financial obligation you owe to the bank. It represents the actual amount borrowed to buy the car. You enter into a loan agreement with the bank, which outlines the repayment terms, including the interest rate, monthly installments, and the duration of the loan. You will need to make regular payments to the bank over the agreed-upon period to repay the debt.

In this example, credit is the financial trust extended to you by the bank, allowing you to borrow the necessary funds to purchase the car. Debt, on the other hand, is the specific amount you owe to the bank as a result of taking the loan. The credit enables you to acquire the car, while the debt is the subsequent financial obligation that arises from borrowing.

After receiving the raw materials on credit, you now have a debt of ₹50,000 to the supplier. This debt represents the financial obligation you owe to the supplier for the materials you received. It signifies the actual amount you borrowed from the supplier to fulfill your business needs. You are now responsible for repaying this debt to the supplier as per the agreed-upon terms, which may include a specific repayment period or payment schedule.

Let’s say you are a freelance coder, and you receive a request from a new client to write a code for their mobile app. The client agrees to pay you ₹20,000 for your services upon completion of the project. Here’s how credit and debt come into play in this scenario:

In this example, credit is the trust placed in you by the client, allowing you to begin the project without receiving payment upfront. Debt, in turn, represents the specific obligation you owe to the client to write the complete the code as agreed. The credit enables you to initiate the project, while the debt represents the subsequent responsibility to fulfill your part of the agreement.

Credit utilization refers to the percentage of your available credit that you are currently using. It is an important factor that impacts your credit score. Let’s consider an example to understand this concept:

A lower credit utilization percentage is generally considered better for your credit score. It indicates that you are not heavily reliant on credit and are managing your debt responsibly. Lenders and credit rating agencies often view lower credit utilization as a sign of good financial management.

Even though both individuals have the same credit limit, Person B has a lower credit utilization, which is more favorable from a credit scoring perspective.

Managing your credit utilization by keeping it low demonstrates responsible credit usage and can positively impact your credit score. It’s generally recommended to aim for a credit utilization rate below 30% to maintain a healthy credit profile.

Remember, credit utilization is just one aspect of credit and debt management, but it can have a significant impact on your creditworthiness and financial well-being.

Here’s a summary of the difference between credit and debt in a tabulated form based on the examples provided:

Examples

Credit

Debt

Example #1: Day-to-Day Life

Borrowing books without upfront payment

Obligation to return borrowed books

Example #2: Credit Card

Accessing credit limit to make a purchase

The specific amount owed to the lender

Example #3: Car Loan

Loan granted to purchase a car

The loan amount disbursed to the borrower

Example #4: Business Purchase

Supply of the raw material without upfront payment

Payment to be made to the supplier

Example #5: Business Sale

The order received from the client is the credit

The Delivery of the complete codes

In each example, credit represents the trust extended or borrowing facility provided, enabling individuals or businesses to access funds, goods, or services. Debt, on the other hand, represents the actual financial obligation resulting from utilizing that credit, indicating the specific amount owed and the responsibility to repay or fulfill the borrowed obligations.

The examples we have examined, whether it’s using a credit card for a purchase, obtaining a car loan, engaging in business transactions, or even borrowing books from a library, demonstrate how credit and debt operate in diverse contexts. They showcase the interplay between credit, which allows individuals or businesses to access resources, and debt, which represents the subsequent responsibility to repay or fulfill the borrowed obligations.

Credit and debt are intertwined but distinct concepts. They play significant roles in personal and business finances, and understanding their implications is key to achieving financial stability and building a strong credit foundation.

Being inspired by the legendary investor Peter Lynch’s investment philosophy, GARP investing combines the best of both growth and value investing. Its aim is to identify companies with strong growth potential at a reasonable valuation.

GARP investing can be defined as an investment approach that seeks to identify companies with robust growth prospects while considering their valuation.

To understand the philosophy behind GARP investing, we turn to Peter Lynch, the renowned investor and former manager of Fidelity Magellan Fund.

Lynch believed in the long-term growth potential of select companies. He emphasized the importance of investing in companies with solid fundamentals. By solid fundamentals, Lynch includes factors like consistent earnings growth, increasing sales figures, and significant market potential.

By focusing on companies with such qualities, Lynch aimed to capitalize on their growth trajectory while maintaining a disciplined approach to valuation.

Assessing a company’s growth potential is a crucial aspect of GARP investing. Historical and projected growth rates are key indicators to consider.

Examining a company’s past performance can provide insights into its ability to generate consistent growth. Additionally, analyzing industry trends and market conditions can help identify sectors with potential for sustained growth.

For example, in the Indian stock market, one such company that demonstrated strong growth potential in recent years is HDFC Bank. With consistent growth in its earnings and an expanding customer base, the bank established itself as a leading player in the Indian banking sector.

Going forward in the year 2023, Indian industries that come under the bigger umbrella of the manufacturing sector look promising. Quality companies operating in the industries like defense, electronic manufacturing, healthcare, renewable energy, logistics, agriculture, etc can see robust growth.

Several factors play a role in evaluating a company’s growth potential. GARP investors consider a company’s competitive advantage, market share, and product differentiation.

A strong competitive position can allow a company to capture market opportunities and maintain its growth trajectory.

For investors like us, the way to forecast future earnings growth rates is to look into the past. We can look at their PAT and EPS numbers in unison.

Note the last 10 years’ PAT and EPS numbers of the company. Plot a line chart for both of them to get a visual trend.

GARP can refer to several different things depending on the context. Here are a few common meanings:

Global Association of Risk Professionals (GARP): GARP is a non-profit organization that focuses on risk management education and certification. It is known for its Financial Risk Manager (FRM) certification program, which is widely recognized in the finance industry. GARP provides resources, research, and a professional network for risk management practitioners.

Generally Accepted Recordkeeping Principles (GARP): GARP is a framework developed by ARMA International (formerly known as the Association of Records Managers and Administrators) to establish guidelines and best practices for effective information and records management within organizations. It outlines principles and standards for the creation, maintenance, and disposition of records.

Glycine Amidinotransferase Reductase Protein (GARP): GARP is a protein that plays a role in various biological processes, including the regulation of immune responses and the development of certain cells. It is involved in T-cell biology and has implications in immune-related diseases.

Generalized Axiomatic Resource Profile (GARP): GARP is a term used in the context of resource allocation and optimization in computer science and network management. It refers to a set of principles or rules that guide how resources are allocated and managed in a system to achieve specific objectives efficiently.

To quantify the trend. We can also calculate the last 10-Yr, 7-Yr, 5-Yr, and 3-Yr growth rates, for both PAT and EPS. The Growth rate (CAGR) formula to be used for calculation is shown below.

Now, compare the PAT and EPS growth numbers.

PAT

EPS

10-Yr Gr.

10.9%

4.1%

7-Yr Gr.

4.86%

-1.60%

5-Yr Gr.

2.73%

-3.54%

3-Yr Gr.

0.29%

0.44%

Digging into the PAT and EPS Growth Rates

Compare the PAT and EPS growth rates. If they are growing at the same pace in all years, it is an ideal growth story.

Explanation (difference in PAT and EPS growth rates)

For some stocks, the PAT growth rate will be higher than EPS growth. It is a situation that will happen only if the company has raised funds by issuing more shares. The number of shares outstanding for such companies grows with time. This in turn reduces the EPS numbers. As an investor, we want outstanding shares to remain constant or better reduce in numbers (shares buyback).

If PAT is growing at a negative rate, then EPS will also show a negative growth rate. Companies showing such characteristics are avoidable.

Note: You can see in the above table, our example stock’s PAT has grown at a slow pace in the last 10 years. But its EPS numbers are either negative or below PAT growth rates. For me, this is a company that is not falling in the investor-friendly range. Though there can be other factors that can fall in its favor. Only a deeper analysis will confirm it.

If PAT is growing but EPS is not growing, it is a case of too much share liquidation. I personally consider this occurrence as a negative indicator, highlighting non-investor-friendly management. Why? Because shares issuance is in the control of the top management. If shares are issued so rampantly that it is causing negative EPS growth, it is not serving the shareholder’s value.

Valuation metrics are crucial in GARP investing as they help determine if a company’s stock is reasonably priced. Commonly used valuation metrics include the price-to-earnings (P/E) ratio, price/earnings-to-growth (PEG) ratio, and price/sales ratio.

These metrics provide insights into a company’s valuation relative to its earnings or sales figures.

P/E Ratio: The P/E ratio is a valuation metric used to assess the relative price of a company’s stock compared to its earnings. It is calculated by dividing the current market price per share by the earnings per share (EPS). A high P/E ratio suggests that investors are willing to pay more for each unit of earnings, indicating a potentially overvalued stock. The high PE of quality companies also indicates that the stock is in high demand.

PEG Ratio: The PEG ratio takes into account a company’s growth rate alongside its P/E ratio. It provides a measure of a stock’s valuation relative to its earnings growth. A PEG ratio below One (1) is generally considered favorable, indicating that the stock may be undervalued relative to its growth prospects.

P/S Ratio: The P/S ratio is a valuation metric that compares a company’s market capitalization to its total sales revenue. It is calculated by dividing the market price per share by the sales per share. The P/S ratio can help assess a company’s valuation compared to its sales performance. A lower P/S ratio may suggest a potentially undervalued stock, while a higher ratio may indicate an overvalued stock.

In GARP investing, finding a “reasonable price” is essential. Peter Lynch emphasized that a reasonable price should take into account a company’s growth prospects and industry norms.

A stock can be considered overvalued if its growth potential does not justify its current price, and conversely, undervalued if its growth potential exceeds market expectations.

An example of this kind is Infosys. The company experienced significant growth during the 2010s, driven by its strong positioning in the IT sector. However, there were instances when the stock became overvalued. It prompted GARP investors to exercise caution and assess whether the price reflected the company’s growth potential.

What we can do more is to analyze the PE number a bit deeper. How? By establishing the PE trend and estimating a forward PE (PE of the future).

For that, we will have to calculate the PE of the last 5 or 10 years. Note the price and EPS data for a 10-Yr time period (as shown below):

Mar ’12

Mar ’13

Mar ’14

Mar ’15

Mar ’16

Mar ’17

Mar ’18

Mar ’19

Mar ’20

Mar ’21

EPS

55.97

65.23

94.17

98.31

117.11

120.04

131.86

80.12

88.64

83.7

Price

589

788

1051

1257

1226

1216

1424

2001

1824

3165

P/E

10.52

12.08

11.16

12.79

10.47

10.13

10.80

24.98

20.58

37.81

Once these two data are available, calculate the PE ratio of the 10 years as tabulated above. Once the calculation is done, we can plot a line chart and establish a trend.

The ideal case will be to see a rising PE. Here we will use a forward PE greater than the current PE (PE-TTM)

In case of a falling trend, we will use a PE that is lower than the current PE (PE-TTM).

The above two steps have established the ‘future earning growth rate’ and ‘Forward PE’. Now, we are ready to confirm if the stock is showing the characteristics of “growth at a reasonable price (GARP)?” How to do it? By calculating the GARP multiple.

PEG Ratio (Let’s call it GARP Multiple)

The lower is the GARP multiple (PEG ratio) the better. If the PEG ratio is below one, the stock’s price is said to be at par with its growth rate. If the PEG ratio is below one, the stock can be said to be undervalued. There is a difference between low PE stocks and GARP stocks. The stocks showing a low GARP multiple may have a high PE ratio, but their PEG will be close to one or below.

Diversification is crucial when constructing a GARP portfolio. By selecting growth stocks from various sectors and industries, investors can mitigate risks associated with individual companies or sectors. GARP investors aim to identify stocks with a combination of solid growth potential and reasonable valuations.

An illustrative example of a GARP portfolio in the Indian context might include companies like HDFC Bank, Asian Paints, and Infosys, which exhibited strong growth potential while maintaining reasonable valuations during certain periods.

Implementing the GARP (Growth at a Reasonable Price) investing strategy involves a series of logical steps that can help investors effectively apply this approach to their portfolio. Here is a breakdown of the process:

Clearly articulate your investment objectives, taking into consideration factors such as risk tolerance, investment horizon, and financial goals. This will provide a foundation for selecting suitable stocks within the GARP framework.

Conduct thorough research to identify companies with strong growth potential in the Indian market. Look for businesses that demonstrate consistent earnings growth, increasing sales figures, and a solid market position. Consider factors such as industry trends, competitive advantage, and product differentiation. Our Stock Engine can be a tool that can help in stock research.

Assess valuation metrics such as the price-to-earnings (P/E) ratio, price/earnings to growth (PEG) ratio, and price/sales (P/S) ratio to determine if a stock is reasonably priced. Compare these metrics to historical data, industry averages, and peer companies to gain insights into a stock’s valuation relative to its growth potential.

Evaluate the quality of a company’s management team and their ability to execute growth strategies. Look for experienced and visionary leaders who have a track record of delivering results. Assess their strategic decisions, capital allocation, and ability to adapt to changing market dynamics.

Build a diversified portfolio of GARP stocks from different sectors and industries. Diversification helps mitigate risks associated with individual stocks or sectors. Allocate funds across companies with varying market capitalizations and growth prospects to balance potential returns and risks.

Continuously monitor the performance of your GARP portfolio. Stay updated with company-specific news, industry developments, and macroeconomic factors that may impact the growth potential and valuation of your holdings. Regularly review your portfolio’s performance against your investment objectives and make adjustments as needed.

GARP investing requires patience and discipline. Avoid making impulsive investment decisions based on short-term market fluctuations. Stick to your investment strategy and give your chosen stocks sufficient time to realize their growth potential. Maintain a long-term perspective and resist the temptation to make frequent changes to your portfolio.

However, it is crucial to conduct thorough research, before buying a potential GARP stock. Generally speaking, GARP stocks trade at a high P/E multiples. Buying at such high PE multiples can be justified only by the stock’s future growth potential. One shall do thorough research on the future growth potential of the stock while practicing GAPR investing.

GARP investing, when executed diligently, can be a valuable tool in an investor’s arsenal, offering the potential for long-term success.

Investors seeking a robust stock screening philosophy can turn to a comprehensive approach based on cash flow, growth, margin, and return. This strategy emphasizes the importanceof positive cash flow from operations, high sales growth, strong gross margin, and superior return on equity (ROE). By evaluating stocks against these parameters, investors can identify companies with solid financials, growth potential, and profitability, enabling them to make informed investment decisions.

The philosophy revolves around the crucial elements of cash flow, growth, margin, and return. By analyzing stocks through these lenses, investors can gain a deeper understanding of a company’s fundamentals.

Next, we’ll delve into the significance of growth, particularly sales growth. Fast-growing sales not only indicate increasing demand for a company’s products or services but also increasing market share.

Finally, our ultimate target is to identify and invest in high-ROE companies. These are companies that generate high returns for their shareholders. But the idea is to identify such companies which will continue to make high ROE in times to come. Hence, we must also analyze the cash flow, margins, and growth aspects of the companies.

Positive net cash flow from operations is a fundamental indicator of a company’s financial health. It represents the cash generated by a company’s core operations. It is cash generated from the sale of goods and services, minus the cash paid for operating expenses.

A positive net cash flow from operations showcases the company’s ability to generate cash internally. This cash flow is vital for its day-to-day operations. Moreover, such cash flows can also be used for investing in growth opportunities and meeting financial obligations.

A company with a strong cash flow can fund its operationswithout relying heavily on external financing. This financial strength provides stability, as the company is less vulnerable to liquidity issues during challenging economic periods.

So, as an investor, our search for fundamentally strong companies should start with the cash flow analysis. This is why, my stock screening philosophy gives it the first priority.

Growth in sales reflects the demand for the company’s products or services. It also shows the company’s focus on its marketing and sales strategies. A combination of good products & services, and effective marketing and sales strategy builds the company’s competitive position. Such companies are more capable of capturing market share.

They may have a competitive advantage that enables them to outperform their peers in terms of revenue expansion. High sales growth can be an encouraging sign for investors, as it suggests the potential for future earnings growth and capital appreciation.

Companies with sustained high sales growth have, on average, experienced higher stock price appreciation and shareholder returns. For instance, D-mart (Avenue Supermart), a retail firm, has achieved an impressive annual sales growth rate of 17% per annum over the past 5-years. This has resulted in a significant increase in the market price of its stocks at the rate of 23% per annum.

One key metric that holds immense importance in assessing a company’s profitability and operational efficiency is the gross margin. Gross margin is calculated by subtracting the cost of goods sold (COGS) from total revenue and then dividing the result by total revenue. It is expressed as a percentage. It represents the proportion of revenue that remains after accounting for the direct costs associated with producing goods or delivering services.

1. Operational Efficiency: A high gross margin suggests that the company is adept at controlling its production costs, optimizing its supply chain, and managing its input expenses effectively. By maintaining a high gross margin, companies can allocate more resources toward research and development, marketing, or expanding their business. It thereby can bolster their long-term growth prospects.

2. Pricing Power: High gross margin often goes hand in hand with a company’s pricing power. Companies that possess unique or differentiated products, strong brand recognition, or a competitive edge in the market. This way they can command higher prices for their offerings. This pricing power allows them to generate more revenue per unit sold, leading to higher margins.

3. Resilience During Economic Downturns: During economic downturns or periods of increased competition, high-margin companies show more resilience. The ability to maintain a healthy margin even in challenging times demonstrates the company’s ability to remain afloat and profitable at all times.

Companies with high gross margins have a competitive advantage and are better positioned to weather industry downturns. A case in point is Grasim Industries, a cement manufacturer. It consistently maintains a gross margin of 65%, above the industry average. This strong gross margin is a result of their premium pricing strategy and operational efficiency. It leads to robust profitability and shareholder value creation.

From the perspective of investors, both Return on Equity (ROE) and Return on Capital Employed (ROCE) are important return ratios. They provide insights into a company’s profitability and efficiency. I personally prefer the use of ROCE. But ROCE is not so easy to calculate and comprehend. Hence, people may also use ROE to do the return analysis.

As an investor, our first preference should be to invest in high ROE and ROCE companies. But some industries have inherently low ROE and ROCE. Does it make these companies bad? No. But if high ROE and ROCE companies are available at better valuation levels, I’ll pick these companies first.

Studies have demonstrated that companies with consistently high ROE and ROCE tend to deliver superior long-term investment returns. An example is Nestle India. The company maintains consistently achieved an ROE of 85% and an ROCE of 50% or higher over the past five years. This remarkable performance is a testament to their efficient capital allocation.

By screening stocks based on the above four metrics, investors can identify companies with strong financials, growth potential, and profitability.

Users can use the Stock Engine’s Big Screener to apply some of the filters discussed above. For example, the big screener can screen stocks on the basis of the following metrics:

Soon, we’ll launch a pre-build screener theme that will exactly filter stocks based on the above four metrics. We’ll name that theme the “4 BIG FILTER.”

In a world marked by financial uncertainties and economic complexities, the pursuit of financial independence has emerged as abeacon of hope. It offers the promise of alife unburdened by monetary constraints. Financial independence is a concept gaining remarkable traction in recent times. It holds the potential to transform lives and empower individuals to breakfree from the rat race.

Imagine a life where you no longer depend on each paycheck to meet your basic needs. Your financial decisions are guided by personal aspirations rather than the constraints of your bank balance. Financial independence paves the way for such a liberating existence, where financial worries take a backseat, and yourfreedom of choice takes the central stage.

But what exactly is financial independence? This is exactly what we’ll discuss in this article. While discussing its benefits you’ll know about its enormity. You’ll know why nearly everyone should make the achievement of financial freedom their primary goal.

The significance of financial independence extends far beyond mere financial stability. It transcends the conventional definition of success. It shifts the focus from the rat race of acquiring possessions to the pursuit of meaningful experiences. By gaining control over your finances, you gain control over your life. This is state of a life where your money works for you, not the other way around.

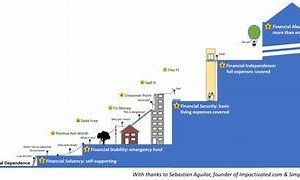

Financial independence is a state where one’s assets generate enough passive income to pay for the required expenses of life. In this state of independence, people need not work (do a job) to earn money. Let me show you an infographic that depicts the state of financial independence.

The state of financial independence can be broken down into five (5) logical steps. It all starts with having an ample size asset base. The accumulated assets will yield returns in the form of passive income. For a financially independent person, this passive income source is large enough to take care of the spending and re-investment needs. Let me explain to you each step briefly:

The Asset Base: In this step, the money is invested and asset accumulation is done over time. The trick is to buy quality assets at an undervalued price. The assets can be stocks, mutual funds, real estate property, bank deposits, annuities, etc.

Return on Asset: The accumulated assets should be capable of yielding regular returns. The returns can be in the form of cash (like dividends, interest, rent, etc) or capital appreciation.

Passive Income: To achieve financial freedom, passive income is the keyword. It is a source of income that continues to yield on its own without our intervention. But to start a stream of passive income, the right assets must be accumulated. If the passive income is big enough, a person can achieve financial freedom.

Required Expense: Let’s take the example of two brothers, one lives in a large city, and the other in a small town. In a large city, the cost of living a comfortable life is say Rs.1,35,000 per month. In a small the cost of living is Rs.50,000. So, to achieve financial freedom, the minimum passive income the two brothers will need is Rs.135000 and 50000 respectively.

Re-Investment: The cost of living increases with time (inflation). Hence, to maintain the state of financial independence, one must re-invest and keep increasing the size of the asset base.

To reach the state of financial freedom, one must never forget the critical step of asset building. Without assets, there will be no passive income hence no freedom from the rat race.

Now that we know about what is financial independence, let’s start to discuss the process of achieving the goal.

There is a process to achieve financial independence. It is a tough goal to achieve, hence following a process will make it comparatively comprehensible. We can divide the process into three stages. It starts with working on the preconditions. Once the preconditions are met, the actual implementation stage will begin. Finally, the goal of financial independence itself can be achieved in stages.

Preconditions: There are a few things that need to be done before attempting to attain financial independence. In this stage, one tries to improve one’s financial health. These improvements in turn help one to climb the peak of financial independence.

Implementation: This is where the core action of asset building & passive income generation is implemented. Here we will discuss how one needs to map the mind to successfully implement the idea of achieving the goal.

Stages of Financial Independence: All financially independent people (families) are not the same. Out of 10,000 people, only one (1) can reach the first stage. Even a lesser number of people (families) can read the second stage. The third stage is rare. Maybe, only one in 10,00,000 can ever reach there. Read more to know what are these stages and how to achieve them.

Let’s start discussing the whole process with stage one, preconditions.

If financial independence represents a house, then these preconditions are the foundation of the house.

The goal of financial independence is such that many aspire to achieve it. But it is no ordinary goal. To achieve this goal, it is necessary to follow a process. If financial independence is the superstructure, then the foundation of this superstructure is the preconditions that we will discuss now.

There are three preconditions that one must take care:

Emergency Fund Creation: The asset purchase should start only after a minimum-size emergency fund is created. The emergency fund consists of three components, cash, life cover, and health cover. The size of each component is linked to one’s monthly expense (E). The cash should be at least six times E. Health coverage should be at least 15 times E, and the life cover should be at least 120 times E.

Cushion Savings: The size of the cushion savings should be at least six times one’s monthly expenses (E). The cash component of the emergency fund will come in handy when emergency strikes. Cushion savings will be used to manage daily expenses. Save your monthly income, instead use cushion savings to manage regular expenses. Use monthly income to replenish the depleted cushion savings. In your mind, the way to manage expenses should look like this.

#4. Implementation of Financial Independence

The above flow chart is a representation showing how one can visualize the implementation of financial independence. Earning money is the first step and then living a frugal life will lead to more savings. Investing the saved money to buy assets can ultimately lead to financial freedom.

Financial freedom is only one goal. In real life, one needs to manage other goals as well. So, one must simultaneously invest to manage other financial goals as well. With this simple mind-mapping, let’s proceed and see the actual implementation process of this step.

In our endeavor toward financial independence, we must learn two things, how to make our income grow continually and frugality. What is Frugal living? Maintaining a lifestyle that is lower than what one can actually afford. Our frugal habits give us the ability to save a majority portion of our income. Combine frugal living with income growth, and it becomes an endless source of savings.

Let’s understand it using an example. Suppose there is a person who earns Rs.100,000 per month. He lives frugally (saving 50% of his income). His income increases by 10% per annum. Let’s see his savings pattern for the next 5 years.

In 5 years the savings of the person rose from Rs.50,000 to Rs.73,205 per month. The person was anyways saving heavily (50%). But as the quantum of savings is increasing every year, its impact on one’s ability to invest is phenomenal.

This is a critical milestone in the journey toward financial freedom. It must be implemented intelligently as equity investing involves a high risk of loss. But if invested properly, equity can yield high returns. In the long term, properly invested money in equity can grow at a rate of 18-20% per annum. One can accumulate equity either by buying stocks directly or through the mutual fund route.

One must continue to buy and hold equity for at least 30-35 years. When quality equity is given such longer holding times, the capital actually begins to compound. For example, investing two lakhs in equity for the next 35 years at 22% per annum will grow to become Rs.20 Crore.

It is advisable to keep two separate asset bases, one for financial independence and the second to manage other financial goals.

In asset base #2, one can keep it well diversified. On one side it can be heavy on quality buy undervalued mid and small-cap stocks. On the other hand, it must also contain non-equity assets like debt funds, bank deposits, gold, REITs, etc.

Breaking down financial independence in stages can help achieve it easily. Financial freedom is a goal that is like a full marathon. One cannot sprint and reach the finish line. It can be achieved only slowly, in stages. There can be three stages of financial independence:

Stage 1 (Basic Independence): In this stage, the passive income generated from assets can fund all basic necessities of life. The basic necessities can be food, clothing, accommodation, utility bills, fees, basic subscriptions, etc. After paying for all these necessary expenses, only little is left to spend on the comforts and even less on the luxuries. For example, in this stage one’s passive income = 1.5x times the basic expense needs.

Stage 2 (Comfort Independence): In this stage, the passive income becomes large enough to take care of all comfort needs. Comfort needs can be like a bigger house, car, etc. It can also be full-time house help, air-conditioned rooms, gymming expense, dining out, entertainment, etc. For example, in this stage one’s passive income => 3x times the basic expense needs.

Stage 3 (Luxury Independence): In this stage, the passive income becomes large enough to take care of the temptations to spend on luxuries. Luxury spending can be big vacations, a posh house, fast cars, binge purchases, etc. For example, in this stage one’s passive income => 10x times the basic expense needs.

So the right strategy will be to put money proportionally in each goal separately. The idea is to keep the goal of financial independence isolated from other goals.

Financial independence can be achieved when “required” income will continue to drip-in even when we are sleeping. We should not be required to work to generate income to manage our expense needs.

Income generated from a job or business is not passive income. It is active income. The idea is to work and generate active income. Then divert at least 50% of the active income to accumulate assets (equity).

But equity accumulation is not enough. It is more important to convert equity into a pure passive income-generating asset. Which are such assets? A few best examples of such assets are the following:

Asset

Passive Income Form

Deposits

Interest

Stocks

Dividend

Real Estate

Rent

Annuity

Pension

Quick Tip:

A sure way of becoming financially independent starts with living a frugal life. Frugality does not mean leading a life of misery. It means, diverting a bigger proportion of one’s income towards the net worth building.

A person who lives a frugal life ensures that a big chunk of his/her income is available as savings. This is a huge advantage. Why? Because this available liquid cash can be used to invest in equity. As equity earns higher returns, over the long term such investments can build a sizeable corpus.

The first part of this corpus shall be used to manage the “other financial goals” of life.

The second part shall be used for “retirement” (financial independence}.

The Credit Utilization Ratio is a crucial aspect of credit scoring. It measures the percentage of available credit a person is using. It is calculated by dividing total credit card balances by the sum of credit limits. For instance, if someone has a credit limit of INR 100,000 and an outstanding balance of INR 30,000, their utilization ratio is 30%.

Understanding Credit Utilization Ratio is crucial for maintaining a healthy credit profile. A good credit profile gives access to better credit opportunities in the future. By keeping credit card balances low and using credit responsibly, individuals can improve their creditworthiness.

In the realm of personal finance, Credit Utilization Ratio is a crucial metric. It reflects the percentage of available credit one utilizes. Understanding and managing credit utilization can significantly impact credit scores. This score can influence lenders’ perceptions of our financial responsibility. By maintaining a low utilization ratio, we showcase prudent credit management, leading to improved creditworthiness. It eventually leads to better credit terms.

The Credit Utilization Ratio is a key metric used in credit scoring that represents the percentage of available credit a person is currently using.

It is calculated by dividing the total outstanding balances on credit accounts by the sum of all credit limits. This ratio offers insights into an individual’s credit management habits and is crucial for evaluating creditworthiness.

The formula for Credit Utilization Ratio: Credit Utilization Ratio = (Total Outstanding Balances) / (Total Credit Limits) * 100 = (30,000) / (100,000) * 100 = 30%

Explanation: In this example, Raj’s Credit Utilization Ratio is 30%. It means he is using 30% of his available credit limit (Rs.100,000). This ratio is calculated by dividing his outstanding balance (Rs.30,000) by the credit limit (Rs.100,000) and then expressed as a percentage.

A Credit Utilization Ratio of 30% or below is generally considered good. It will positively impact Raj’s credit score. It indicates that he is using credit responsibly and not maxing out his credit card. Keeping the Credit Utilization Ratio low is a prudent financial practice.

Credit utilization is a crucial factor in credit scoring because it reflects how responsibly someone manages their credit. It’s simply the percentage of credit they’re using compared to the total credit they have available. A high credit utilization ratio, meaning they’re using a large portion of their credit, can negatively impact their credit score. This is because it suggests they may be relying too much on credit. The logic is that if a person’s income-to-expense ratio is low, he will have to dig into his credit to manage expenses.

On the other hand, a low credit utilization ratio, where they’re using only a small part of their credit, can positively affect their credit score. This indicates that the person has a high income-to-expense ratio. Lenders like to see low utilization because it shows they’re not taking on too much debt and are less likely to be a risky borrower.

Statistics vividly highlight the importance of maintaining a healthy credit utilization ratio.

For instance, individuals with a low utilization ratio (below 30%) tend to have higher credit scores. It makes them more likely to qualify for favorable interest rates on loans and credit cards.

On the other hand, those with high utilization ratios may face difficulties obtaining credit or end up paying higher interest rates.

Statistics reveal a strong correlation between responsible credit utilization and improved financial well-being. This underscores the need to manage credit wisely to secure a brighter and more stable financial future.

Suppose there is a person who carries two credit cards. We’ll see how the credit utilization ratio is calculated in this case. Let me give you the actual case in consideration.

The First Card has a credit history of 10 years. Its credit limit is Rs.10 Lakhs. Generally, the person maintains a credit limit of 15% on this card.

The Second Card has a credit history of only a month. Its credit limit is Rs.1.4 Lakhs. Generally, the person maintains a credit limit of 70% on this card.

We’ll use this example to learn to calculate the credit utilization ratio of a person carrying multiple credit cards. Moreover, we’ll also use this example to bring forth the case of wise credit management.

But first, let’s learn to calculate the utilization ratio of multiple cards.